Investors

If you have already invested in the protocol, consult your investment here.

Demystifying the Crypto Market.

Crypto is not about getting rich quick, it's about understanding where the financial world is evolving and not being left behind.

1. Technology, not just speculation. Crypto is not just "digital currency," it's a technological infrastructure (blockchain) that allows the transfer of value, data, and ownership without intermediaries.

2. Institutional and real-world adoption.

Banks, governments, and companies are already using or testing crypto/blockchain (payments, tokenized securities, stablecoins). The traditional financial sector has already realized the potential of crypto.

Banks and Financial Institutions

- JP Morgan created its own blockchain (Onyx) and the stablecoin JPM Coin, used by institutional clients for real-time settlements.

- Goldman Sachs is already trading Bitcoin derivatives and exploring asset tokenization.

- BlackRock the world's largest asset manager; launched Bitcoin ETFs and is studying tokenization products.

- Fidelity offers custody and trading of Bitcoin and Ethereum to institutional clients.

- Banco Santander has already issued tokenized bonds on the blockchain.

- BNY Mellon offers crypto custody services for institutional investors.

3. Transparency and control. Unlike the traditional financial system, the blockchain is public, transparent, and auditable by anyone.

4. The total market value of cryptocurrencies is around US$ 4.16 billion (≈ US$ 4.16 trillion). The nominal GDP of Portugal in 2024 was about US$ 309 billion. Even though it is a volatile market and not equivalent to the "real value" of productive assets, it shows that the crypto market already represents a magnitude that surpasses the economy of medium-sized countries like Portugal, in this case 13 times the value of the national GDP.

5. In Europe, the MiCA regulation has brought clarity for companies and investors, allowing traditional banks to offer regulated and secure alternatives to the public regarding crypto asset investments.

US Legislation

Bank Of America

Charts - Historical data of the protocol.

Total investment in the protocol (million dollars).

Colend Protocol TVL

USDT

Pool 1 Base Supply APY

USDC

Pool 2 Base Supply APY

Source: Defillama.

How to Invest

Investment in dollars (Stable Coin*):

50% USDT / 50% USDC

MPY (monthly interest): 1%

APY (annual interest): 12%

Kraken - Stable Coins Market.

Investment Details

Method

- Investment in the protocol in a 50% USDT/50% USDC ratio, guaranteeing a net profit return (yield) of 1% monthly (MPY) and 12% annually (APY) based on historical data.

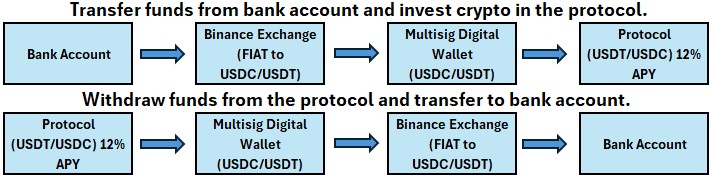

- Creation of a TokenPocket digital wallet for fund allocation. The investor transfers the funds to a Multisig wallet, which is a Token Pocket digital wallet that requires two signatures to perform any operation, one from the investor and one from the investment manager.

- Mobilizable funds; the investor can withdraw the funds at any time with 24 hours' prior notice. Note that the investment must be held for a minimum of 30 days to receive the interest, as the interest is accumulated daily.

- Monthly payments or compounding interest.

- 24/7 online access to invested funds.

- There are no associated deadlines for the investment; the investor has total flexibility in the period they wish to invest.

Investment Flow Chart

90-day Investments.

Withdrawals every 30 days.

| Capital | Days | Yield | Profit | Total |

|---|---|---|---|---|

| 10000.00 | 30 | 0.01 | 100.00 | 10100.00 |

| 10000.00 | 30 | 0.01 | 100.00 | 10100.00 |

| 10000.00 | 30 | 0.01 | 100.00 | 10100.00 |

Total after 90 days: 300.00 → 10300.00 (3.00%).

Annual Total 11200 (12% APY).

Withdrawal at 90 days.

| Capital | Days | Yield | Profit | Total |

|---|---|---|---|---|

| 10000.00 | 30 | 0.01 | 100.00 | 10100.00 |

| 10100.00 | 30 | 0.01 | 101.00 | 10201.00 |

| 10201.00 | 30 | 0.01 | 102.01 | 10303.01 |

Total after 90 days: 303.01 → 10303.01 (3.031%).

Annual Total 11268.25 (12.68% APY).

Multisig Wallet TokenPocket

What the multi-signature digital wallet proposes to do is the solution for when an operation is intended to be performed by more than one individual in a group.

Single-signature Wallet

A single-signature wallet is the most common type of wallet. To perform a transfer operation on the blockchain, it is necessary to generate a signature with the wallet. The user signs and sends the transaction, and the operation is completed.

Multi-signature Wallet

As the name suggests, it is a wallet that requires several people to sign to perform an operation. To transfer funds from a multi-signature wallet, it is necessary for M out of N people to sign and send the transaction for the operation to be completed.

- M represents the number of necessary signatures.

- N represents the total number of people in the group.

For example, in 2/3 signature mode, two of the three people in the group need to sign the transaction for it to be executed.

Where and How it is Used

Multi-signature technology on networks like ETH and EVM-compatible chains (like BSC/BEP20) is implemented through a smart contract.

Application Scenarios:

- Asset Management by Multiple People: Ideal for companies or groups that manage assets together, preventing fund diversion by a single individual.

- Enhanced Security: Increases asset security, as it requires multiple private keys for a transaction.

- Other Security Scenarios: Applies to any situation where shared security and trust are crucial.

Protocol Audits

Risks - Questions & Answers

- Q - Can I lose the funds invested in the protocol?

R - There is always a possibility, although very small, that the protocol could be hacked and the funds in the pool drained. This particular protocol has been subject to FOUR audits carried out by the most reputable "smart contract" audit companies on the blockchain, and no vulnerabilities were found, offering extreme security robustness (see the table above). - Q - Even considering that the protocol has been subjected to several audits and is extremely secure, how can I eliminate 100% of the risk?

R - For total capital security, the investor can choose to insure the investment with a monthly cost of ~0.25%/month of the capital on the OpenCover platform, which supports more than 80 protocols and covers 100% of the capital, but will reduce the monthly return from 1% to ~0.75%. - Q - Is it possible for the investment manager to transfer the funds from the protocol to a personal wallet?

R - Impossible. When the investment is made in the protocol, the wallet that provides the funds is associated with the "smart contract" and only that wallet has access to the funds. For the funds to be withdrawn, the investor must sign one of the two wallet signatures. The investor will always be aware of any fund transaction and must give their consent for the transaction to be carried out. - Q: The historical data shows an APY above 12%, so why do I only receive 12% interest?

A: The APY exceeding 12% represents the profit margin of the investment manager. For example, if in a certain 30-day period the APY was 16%, the amount exceeding 12% (i.e., the extra 4%) will be transferred to the investment manager’s wallet, leaving in the protocol only the invested amount plus 1% corresponding to the previous 30-day period. - Q - What is the ISSR (Summary Indicator of Risk and Return) rating for the investment?

R - The ISSR rating for the investment risk is 2 (only the exchange rate). If the investment capital is insured and at the time of withdrawal the dollar to another currency exchange rate is favorable compared to the exchange rate at the time of investment, then the risk will be 1. If the bank curremcy is in dollars no risk is associated with the investment.